By Alvin Camba

As a cornerstone project by President Joko “Jokowi” Widodo, the Jakarta-Bandung high speed railway (HSR) has often been featured in analysis of the Belt and Road Initiative. Like many major Chinese projects in the global south, this project has been labelled a “debt trap” and politicized during elections.

One investment in Indonesia that has received scant attention, however, is the Indonesia Morowali Industrial Park (IMIP), a joint venture between Tsingshan, a Chinese provincial state-owned enterprise, and Bintang Delapan, a domestic Indonesian firm. With Indonesia’s current National Medium Term Development Plan period (2020-24) expected to see the construction of an additional 27 industrial parks, many of which are likely to see Chinese involvement, such joint ventures are certainly deserving of analysis.

The HSR provides a case of host country elites attaining leverage due to competing investors, allowing those elites to attain political legitimacy and access easy money despite the ramifications on the financial health of the country. In contrast, the IMIP, which is directly tied to nickel processing, illustrates how a host country’s industrial policy, which has developmental goals such as upgrading a country’s technological base, disproportionally benefits certain firms and subsectors at the expense of others. In the case of IMIP, capital-intensive smelters have benefited enormously, while mining firms have suffered, resulting in massive social and environmental costs. Recent analysis of IMIP focuses on the issue of Chinese workers and environmental ramifications in the park. However, IMIP is not only a case of a single park, but also an instance of selective government policies that prioritize one subsector over another.

Chinese investments in nickel processing, which is largely represented by IMIP, has created an oligopsony – a situation in which numerous suppliers are forced to compete for relatively few buyers – for firms with smelters.

Oligopsony:

a market situation in which each of a few buyers exerts a disproportionate influence on the market (Merriam-Webster Dictionary)

In other words, Indonesia’s domestic mining companies now compete for access to their primary customer, smelting firms, many of which rely on the backing of Chinese capital in the form of joint ventures. Indonesian policy elites are attempting to increase industrial capacity by discouraging primary commodity exports, particularly raw nickel extracts, to foreign markets. These elites have done so by imposing a nickel export ban, which Chinese firms capitalize on by establishing nickel smelters in Indonesia through joint ventures with several Indonesian large-scale mining (LSM) firms. The ban primarily inhibits LSM firms and artisanal small-scale mining (ASM) groups from selling to foreign markets, allowing the newly relocated Chinese smelting firms with huge smelting and processing capacity to dominate the demand side and dictate the nickel price at very cheap rates. In response to this inadvertently created oligopsony, LSM firms and ASM groups are cutting corners in order to make up for lost profit, passing socio-environmental costs onto Indonesian communities and environments.

Industrialization and Chinese Nickel Smelting Firms

Indonesian political and policy elites are cognizant of Indonesia’s reliance on exporting primary commodities, such as coal, base and precious metals, and palm oil. Since the Cold War, these elites have created numerous initiatives to encourage domestic industrial capacity by providing incentives, limiting imports, and banning some form of natural resource exports. Like many countries in the global south, Indonesia has followed a policy of establishing special economic zones (SEZ) and their various iterations to encourage foreign transfer of skills and technology. However, SEZs, conventionally from Western firms, have been criticized as perpetuating the two-tier economy; one comprising the foreign funder firms and their high-value industries, and the other lower-tier host country economy that provides cheap labor and other primary inputs to the firms.

Chinese firms building their own SEZs in the global south is becoming a new development trend. Data indicates that there are over 99 Chinese-funded overseas parks in the global south. In one famous case, the Malaysia-China Kuantan Industrial Park (MCKIP) was established to circumvent Western tariffs for Alliance Steel, a private Chinese firm, capitalizing on importing Australian ore and assembling steel exports in the area. Similarly, Chinese industrial parks in Thailand, Ethiopia, and Nigeria give incentives to firms to invest, generate local employment, and relocate production in the respective host countries.

Indonesian policy elites want to establish industrial parks not only to increase investments, but also to generate technology and skill spillovers in the hopes of reducing the country’s reliance on natural resource exports. The Tsingshan Group, one of the largest private stainless-steel manufacturers in China with significant linkages to the Zhejiang provincial government, formed a partnership with Bintang Delapan, one of Indonesia’s largest nickel mining companies, and the Indonesian government to build the IMIP in the Morowali Regency in 2012. The China-based Shanghai Decent Investment, a company in the Tsingshan Group, owns 66.25 % while Bintang Delapan Group owns 33.75% of IMIP. IMIP is the first integrated steel facility in Indonesia, comprising an airport, stainless steel facilities, mineral processing plants, and a port. IMIP spans 5000 hectares and comprises 43,000 workers, divided into 38,000 Indonesian workers and 5,000 imported Chinese ones.

Tsingshan and Bintang Delapan also established the Sulawesi Mineral Investments (SMI), which is IMIP’s “extraction arm.” SMI covers old mineral concessions from Bintang Delapan as well as newly-acquired ones, sending freshly-extracted nickel to IMIP for the smelting process. IMIP not only purchases nickel from SMI, but also from the LSM firms and ASM groups in Sulawesi and the whole country. Prior to IMIP, Tsingshan’s business model was to import nickel from Sulawesi to use in its stainless steel production in China, much of which was then exported to Southeast Asia, Europe, and North America.

Building an integrated industrial park gave Tsingshan a significant cost reduction by moving processing from China to Sulawesi, tapping into cheap Indonesian labor, and shortcutting lengthy bureaucratic procedures in both countries. Most importantly, investing in Indonesia gave Tsingshan guaranteed access to the nickel concessions through SMI, which would insulate production from international price fluctuations, political disputes, and the likelihood of export bans. Additionally, Tsingshan could also purchase nickel from LSM firms and ASM groups across the country.

A number of other Chinese firms have invested in smelters over the last decade, such as the Delong Group, which formed Virtue Dragon Nickel Indonesia (VDNI) in Southern Sulawesi. In 2012, Delong investment holding made a $6 billion greenfield investment at Konawe regency, comprising a stainless-steel plant, nickel processing facilities, and a port. VDMI’s smelting capacity is similar to IMIP, making it the second major domestic buyer of nickel.

In 2019, Indonesian president Widodo signed a presidential decree on providing incentives to investments in electric vehicles, aiming to take advantage of the country’s abundance of nickel, cobalt, lithium, graphite, and rare earth elements. IMIP, VDMI, and the Indonesian government are anticipating a surge in the global demand for electric vehicle batteries. Indeed, Tesla is already in the early stages of investment negotiations with the Indonesian government. Chinese firms such as Huadi Steel Group, mining and metallurgy group Jinchuan, Huayou Cobalt and Zhensi Steel all took the decree as a signal and have become involved in industrial projects such as the Indonesia Weda Bay Industrial Park.

Export Ban and Oligopsony

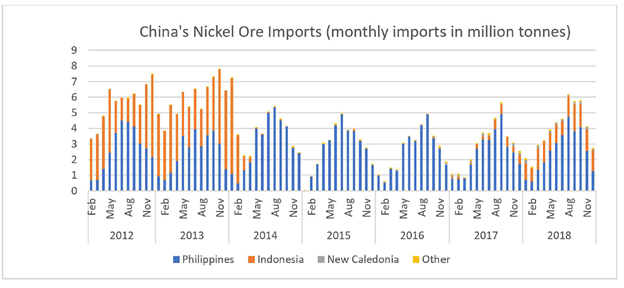

In 2009 President Susilio Bambang Yudhoyono (2004-2014) instituted a ban on exporting unprocessed low-grade nickel. As seen in figure 1, Indonesia was China’s source of nickel imports until 2013. After the nickel ban was imposed in 2014, Indonesia’s nickel exports dropped, pushing Indonesian miners to sell to IMIP, VDNI, and other smelting firms at very low rates. The ban was slightly relaxed in 2017 to 2018, as evident in China’s nickel import numbers in Fig. 1, but reimposed at the end of 2019.

Yudhoyono’s Law 4/2009 on Mineral and Coal Mining intended to increase domestic nickel processing capacity by allocating state financing to help LSM nickel firms build smelting facilities, thereby reducing Indonesia’s dependency on natural resource exports. But the law initially did not substantially change nickel mining because only several firms could afford their own smelters. After a change of administration in 2014, Jokowi relentlessly pursued the Chinese state to fund the upgrade of Indonesia’s industrial capacity. A key part of the investment incentive is for the Chinese firms to “exclusively” access the domestic nickel supply in exchange for investments in processing technologies.

Law 4/2009 also newly permitted Indonesian provincial governments and the regents to grant mineral concessions to LSM firms and ASM groups. In other words, a variety of state units – regional governments, governor, and regency – differentially determine which areas can be designated for mining and which market players to allow. The change in permitting powers led to a rapid expansion of LSM firms and ASM groups in the country as local authorities chased mining projects. According to an Indonesia Investment Cooperation Board (BKPM) official interviewed in 2019, Indonesia already had thousands of licensed LSM and ASM groups, including many unregulated ASM groups, pushing extraction beyond the government’s oversight capacity.

Smelting firms have taken advantage of this. The sheer number of regulated and unregulated LSM firms and ASM groups created a race to the bottom to compete for the limited domestic nickel market, allowing the smelting firms to pushdown the price. While the Indonesian government established a domestic price, which is cheaper than the international index, smelting firms circumvent government regulations in order to impose their own price cheaper than the one dictated by the government. To make up for lost profits, LSM firms and ASM groups inevitably resort to cutting corners, limiting environmental impact assessment, reclamation, and dumping. Indeed, a study in Sulawesi indicates that nickel and heavy metal pollution in Sulawesi is 20 times more than the government anticipated.

The sheer number of regulated and unregulated LSM firms and ASM groups created a race to the bottom… To make up for lost profits, LSM firms and ASM groups inevitably resort to cutting corners, limiting environmental impact assessment, reclamation, and dumping.

Indonesian LSM firms and ASM groups have tried to convince the government to remove the ban. In April last year, the Indonesia Nickel Miner’s Association set up a meeting with the Jokowi administration to remove the ban. However, the ban remains in place. The government responded by pushing a strongly worded regulation, tightening the domestic-sanctioned price, and allowing some limited form of exports for some mining firms. Smelting firms, capitalizing on the oligopsony, are still reportedly taking advantage of the situation due to limited regulations.

Chinese investment in IMIP illustrates how a host country’s industrial policies, which sought to increase a country’s technological base and world-economic position, resulted in vastly benefiting one set of market actors – Chinese firms and their Indonesian partners with smelters and mines – over others. While analysis on the Belt and Road often focuses on how host country elites could play one set of investors against another – Japan versus China in Jakarta-Bandung HSR – the IMIP case illustrates a “triple alliance” between the Indonesian political elites, Chinese investors, and the domestic Indonesian firms. Analyzing alliances gives greater purchase to understanding the Belt and Road Initiative and the internationalization of Chinese firms as new relationships and networks are formed, pitting host country elites and firms against one another. Rather than a division between investor and host country actors, the competition between the alliances of Chinese firms and host country elites against coalitions within the host country is often the most interesting aspect of Belt and Road investments. The Indonesia Morowali Industrial Park illustrates the playing out of such dynamics.

This blog is based on a recently published paper in Extractive Industries and Society: Camba, A., Tritto, A., & Silaban, M. (2020). From the postwar era to intensified Chinese intervention: Variegated extractive regimes in the Philippines and Indonesia. The Extractive Industries and Society, 7(3), 1054-1065. https://doi.org/10.1016/j.exis.2020.07.008

Alvin Camba is a PhD Candidate in Sociology at Johns Hopkins University, focusing on international political economy, development sociology, and environmental change. He works on Chinese capital inflows, elite collective action, and contentious politics in maritime Southeast Asia. His future projects examine illicit capital and the coal-cement-infrastructure interface.